Europe’s AI Problem

Despite all the conferences, strategy papers, funding announcements and speeches about AI sovereignty, Europe is very poorly positioned in the global world of artificial intelligence. We have no Nvidia in semiconductor chips, no Google, Amazon or Microsoft in cloud services, no OpenAI or Anthropic at the frontier model layer and we have no global consumer platforms like Apple. To make matters worse, we do not have the depth of capital markets that the United States has and to make things even worse, we are drowning in bureaucracy that slows down AI adoption, restricts experimentation and makes it far too difficult to build the necessary energy, grid and data centre infrastructure to compete in the age of intelligence. That is the negative part but it does not mean all is lost for Europe. What it does mean is that Europe needs to stop pretending that good intentions, some EU regulations and a handful of promising startups are enough as they are not. Instead, Europe needs a clear strategy with a real action plan behind it to catch up in what is probably the most important technology shift in the history of mankind.

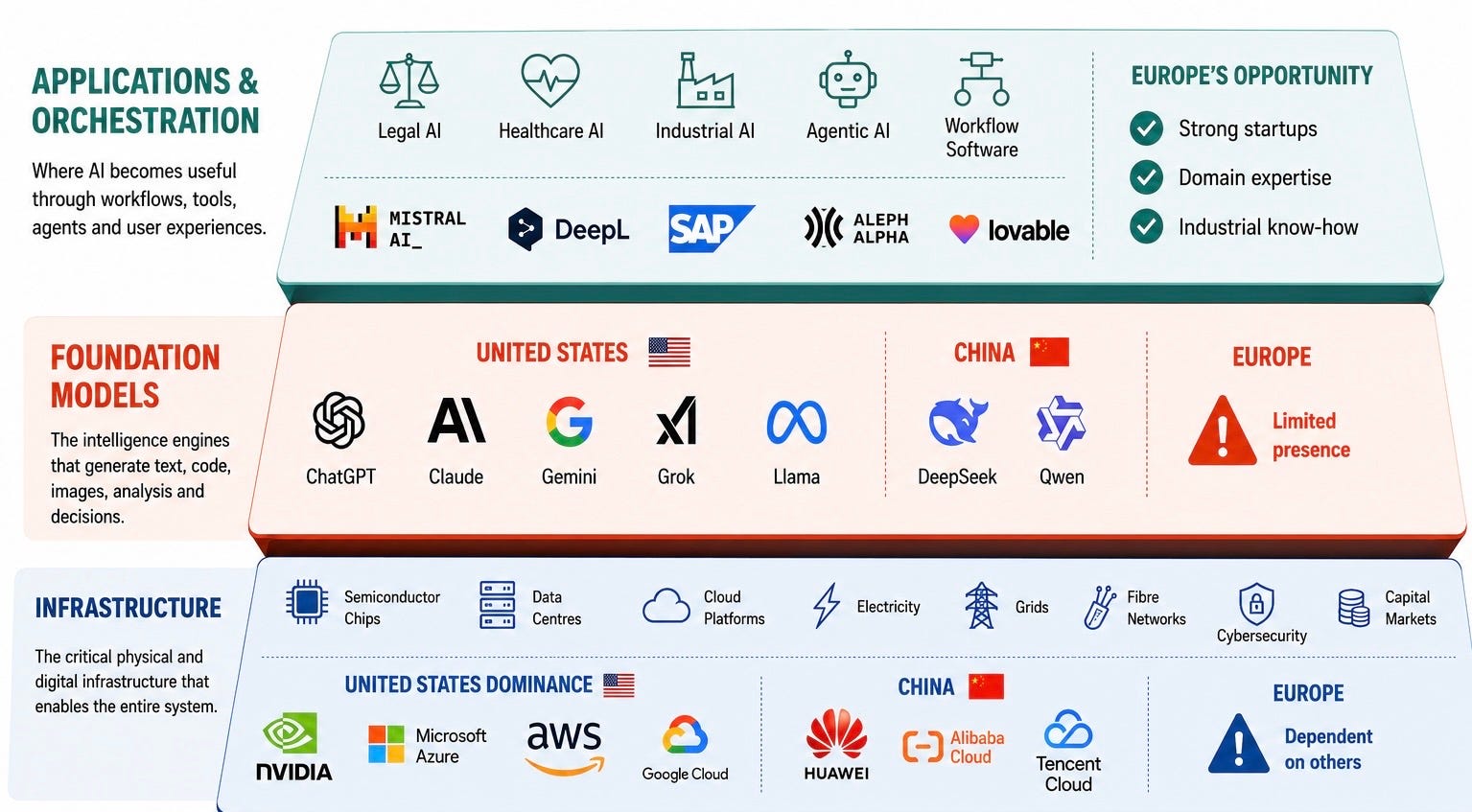

To give some context, it is useful to think about AI in three layers, the first of which is the infrastructure layer which is the critical infrastruture that enables the whole system such as semiconductor chips, cloud, compute, data centres, power electronics, electrical infrastructure, cooling, fibre, cybersecurity and financial capital. The second layer is the frontier model layer which are the intelligence engines such as GPT, Claude, Gemini, Grok, Llama and DeepSeek that generate text, code, images, analysis and decisions. The third layer is the application and orchestration layer which is where the model is turned into something useful which includes the user interface, instructions, tools, memory, workflows, agents, data connections, permissions and integrations that allow AI to be used by end customers.

What I continually here in Europe is that we do not need to compete at the frontier model layer of AI as it is too expensive, too risky and too capital intensive with major players such as ChatGPT, Claude and Gemini in the United States and Deep Seek in China too far ahead. Instead, the argument goes, Europe should focus on the application and orchestration layer, where AI becomes useful, where workflows are transformed, where customers are won and where companies can be built quickly with less capital. There is a lot of truth in this and I agree that Europe absolutely must build AI applications which are the tools that doctors, engineers, lawyers, teachers, financiers, architects, grid operators and factory managers will use to improve productivity, reduce costs and improve the quality of their services and products. But the question is whether many of these application software businesses are truly defensible if they depend on the very same companies that provide the foundational models, cloud infrastructure and distribution platforms beneath them.

Cases in point: Robin AI, the UK legal AI company and their US peer Harvey both of which built their legal AI platforms around Anthropic’s Claude models, only for Anthropic this year to release a competitive product Claude Legal. The uncomfortable lesson from this is that your AI supplier may become your competitor, or change the rules or pricing to put your nice applications business under serious pressure. The same risk exists across coding assistants, agent builders, productivity tools, financial software and industrial AI applications and the reality is the more valuable an application becomes, the greater the incentive for the model provider or hyperscaler to move into that space and compete with their customers.

There is, however, an important counterargument and that is you do not need to own the model if you own the setup around the model. With this view, the model is rented, but the application, instructions, tools, workflows, memory, data connections, integrations, permissions and user experience are owned. As AI becomes more advanced, this orchestration layer will matter enormously. Standards such as MCP for connecting models to tools, files, databases and APIs, and A2A for communication between agents, could make it easier to switch between models and reduce dependency on any single provider. This matters, and Europe should take it seriously. Model independent infrastructure could become a major European opportunity which means that Europe should build the tools, memory systems, agent frameworks, data connectors, identity layers, security systems and workflow engines that allow companies to use different models without being trapped inside one ecosystem. But we should not confuse this with sovereignty.

The recent restriction by the US government on the use of Anthropic’s Fable 5 and Mythos 5 models by non-US residents shows why soverignty matters and this is a critical point for Europe to understand. If your AI application depends on a foreign model, your supply chain includes the politics of the country that controls that model. You may own the wrapper, the workflow, the customer relationship and the data connections, but if the model beneath you can be switched off, restricted or repriced by forces outside your control, then you do not have sovereignty and instead have a massive business and geopolitical risk.

The infrastructure layer is the basis on which AI foundation models as well as the application and orchestrational layers sit and again Europe is weak here with the semiconductor chips and computing power coming from the US, not to mention cloud infrastructure and the ownership of the majority of European based data centers. The good news is that Europe does have a good electrical infrastructure and lots of excellent firms like ABB and Schneider that provide critical electrical components to global data center players. And this is the area where Europe needs to build on as AI is exceptionally electricity hungry, infrastructure intensive and capital intensive.

This matters because AI is not simply a software revolution but also an electricity revolution. Every AI query consumes electricity as does model training and the use of AI agents, all of which require servers, cooling systems and networks. The countries that can provide abundant, reliable and low cost electricity will increasingly attract AI investment, data centres and advanced manufacturing.

Capital is equally important when it comes to the infrastructure layer. The United States did not become the global leader in AI simply because it built better technology. It did so because it has the deepest venture capital market, the strongest growth equity ecosystem and the largest public capital markets in the world. Capital is part of the AI infrastructure stack because without it companies cannot scale and Europe’s fragmented capital markets remain one of its biggest structural disadvantages.

Finally, Europe has no shortage of talented entrepreneurs, engineers or researchers. What it lacks is a coherent strategy that connects electricity, infrastructure, technology and capital into a single industrial vision. Too often we discuss AI as though it were simply another software industry. It is not. AI is becoming as important to the 21st century economy as oil was to the 20th. The countries that control the full stack will capture the economic value, the industrial capability and ultimately the geopolitical power that comes with it. Europe still has time to compete, but only if it starts thinking about AI as an infrastructure revolution more than as a software revolution. The obvious question then becomes what should Europe actually do and that is the subject of my next article.